The 2-Minute Rule for Chapter 7 Vs Chapter 13 Bankruptcy

Table of ContentsNot known Factual Statements About Experienced Bankruptcy Lawyer Tulsa The Ultimate Guide To Bankruptcy Attorney Near Me TulsaSome Known Details About Bankruptcy Law Firm Tulsa Ok Some Known Details About Affordable Bankruptcy Lawyer Tulsa Some Known Facts About Tulsa Debt Relief Attorney.

The statistics for the various other major kind, Phase 13, are even worse for pro se filers. (We damage down the differences between both enters depth listed below.) Suffice it to say, talk with an attorney or 2 near you that's experienced with bankruptcy law. Right here are a few resources to locate them: It's reasonable that you might be hesitant to pay for a lawyer when you're already under substantial financial pressure.Numerous attorneys likewise offer free examinations or email Q&A s. Make the most of that. (The non-profit application Upsolve can assist you discover complimentary consultations, sources and lawful help release of fee.) Ask them if bankruptcy is without a doubt the best choice for your situation and whether they assume you'll certify. Before you pay to file insolvency types and blemish your credit score record for approximately one decade, inspect to see if you have any kind of practical options like financial obligation settlement or non-profit credit report counseling.

Advertisement Currently that you have actually made a decision insolvency is certainly the best program of activity and you ideally cleared it with an attorney you'll require to obtain started on the paperwork. Prior to you dive right into all the main personal bankruptcy forms, you must obtain your very own files in order.

See This Report about Bankruptcy Lawyer Tulsa

Later on down the line, you'll in fact require to show that by divulging all kind of information regarding your financial events. Here's a basic listing of what you'll require when driving in advance: Recognizing documents like your chauffeur's permit and Social Protection card Tax obligation returns (up to the past 4 years) Proof of income (pay stubs, W-2s, freelance earnings, earnings from properties along with any earnings from federal government benefits) Bank statements and/or retirement account statements Evidence of worth of your assets, such as vehicle and genuine estate appraisal.

You'll intend to recognize what kind of financial obligation you're trying to settle. Financial obligations like child Tulsa bankruptcy attorney support, spousal support and particular tax financial debts can't be discharged (and personal bankruptcy can not stop wage garnishment related to those debts). Trainee funding debt, on the other hand, is not difficult to discharge, yet keep in mind that it is tough to do so (Tulsa bankruptcy lawyer).

You'll intend to recognize what kind of financial obligation you're trying to settle. Financial obligations like child Tulsa bankruptcy attorney support, spousal support and particular tax financial debts can't be discharged (and personal bankruptcy can not stop wage garnishment related to those debts). Trainee funding debt, on the other hand, is not difficult to discharge, yet keep in mind that it is tough to do so (Tulsa bankruptcy lawyer).If your income is expensive, you have another choice: Phase 13. This choice takes longer to solve your financial obligations since it needs a lasting settlement strategy normally three to 5 years prior to some of your continuing to be financial obligations are cleaned away. The declaring process is likewise a lot much more complex than Chapter 7.

8 Simple Techniques For Chapter 7 Vs Chapter 13 Bankruptcy

A Phase 7 bankruptcy stays on your credit history record for 10 years, whereas a Phase 13 bankruptcy diminishes after seven. Both have lasting impacts on your credit rating, and any type of brand-new debt you get will likely feature greater rate of interest prices. Prior to you send your bankruptcy forms, you should initially finish an obligatory training course from a credit report counseling agency that has actually been approved by the Division of Justice (with the noteworthy exemption of filers in Alabama or North Carolina).

The program can be finished online, in person or over the phone. You should finish the program within 180 days of filing for personal bankruptcy.

The Best Strategy To Use For Experienced Bankruptcy Lawyer Tulsa

Inspect that you're submitting with the proper one based on where you live. If your irreversible residence has relocated within 180 days of filling, you should submit in the area where you lived the greater portion of that 180-day duration.

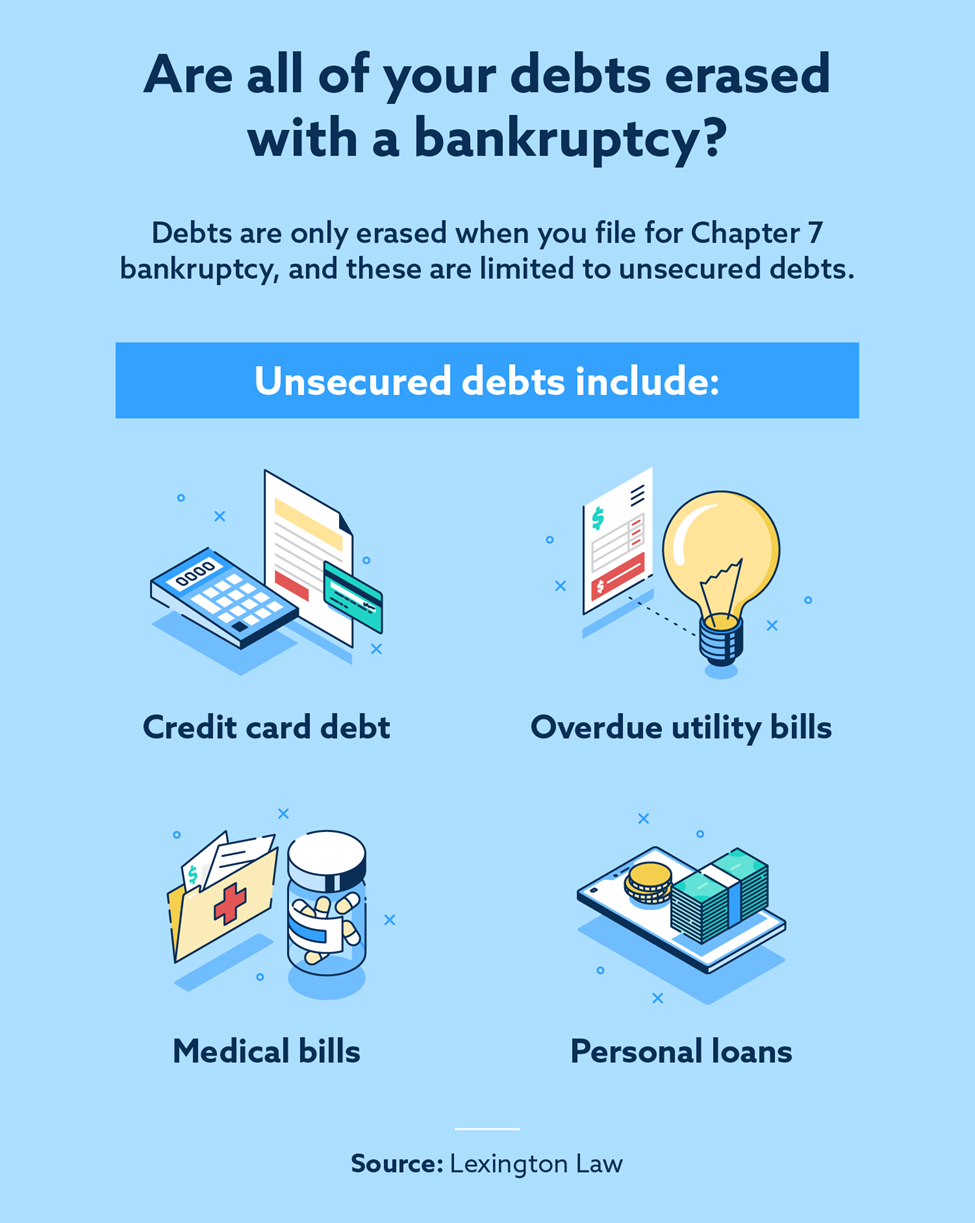

Normally, your insolvency attorney will function with the trustee, yet you might require to send the individual documents such as pay stubs, tax obligation returns, and bank account and credit history card statements directly. A common misconception with bankruptcy is that once you file, you can stop paying your financial obligations. While personal bankruptcy can assist you wipe out several of your unprotected financial obligations, such as overdue clinical expenses or personal lendings, you'll want to maintain paying your regular monthly payments for protected financial debts if you want to keep the residential or commercial property.

Rumored Buzz on Best Bankruptcy Attorney Tulsa

If you go to danger of repossession and have exhausted all other financial-relief choices, then applying for Phase 13 may postpone the repossession and conserve your home. Ultimately, you will still need the revenue to proceed making future home loan settlements, along with paying off any type of late payments over the click resources course of your payment plan.

The audit could delay any financial obligation alleviation by a number of weeks. That you made it this far in the process is a suitable indicator at the very least some of your financial obligations are qualified for discharge.